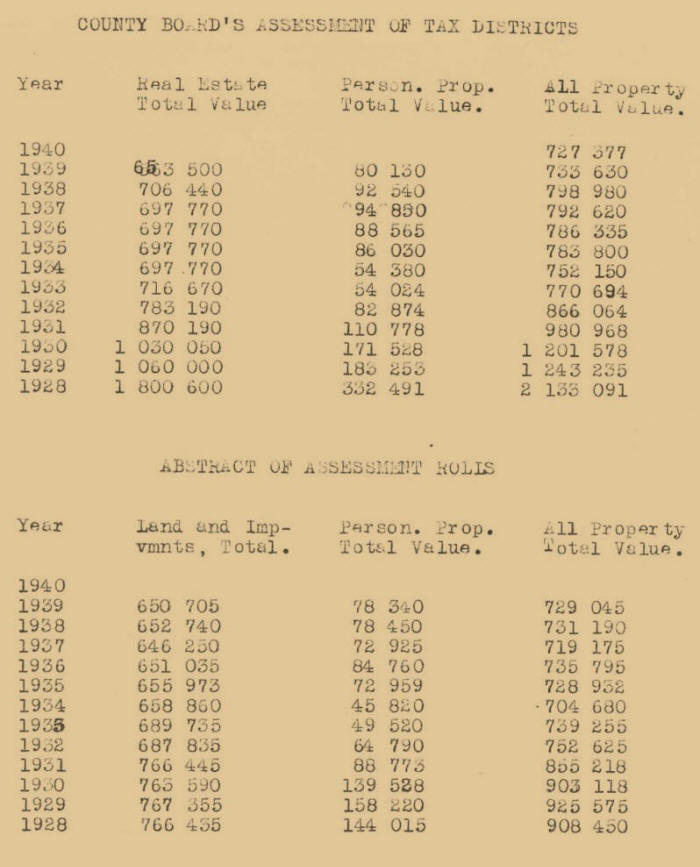

TEN YEARS OF TAXATION IN THE TOWN OF MENTOR

by Wayland B. Waters, Madison, Wisconsin, January, 1941

Part II

Handwritten Pages

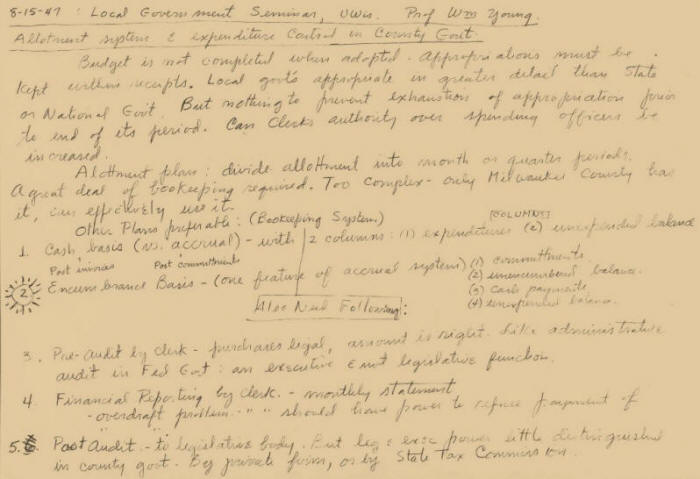

8-15-47 – Local Government Seminar, U-Wis. Prof. Wm. Young

Allotment system & expenditures in County Gov’t

Budget is not completed when adopted. Appropriations must be kept within receipts. Local gov’ts appropriate in greater detail than State or National Gov’t. But nothing to prevent exhaustion of appropriation first to end of its period. Cty Clerks authority over spending officers to be increased

Allotment plan: divide allotment into month or quarter periods; a great deal of bookkeeping required; too complex, only Milwaukee County has it, can effectively use it.

Other plans preferable – (Bookkeeping system)

Cash basis (no accrual) with 2 columns: (1) Expenditures (2) Unexpended balance

2. Encumbrance Basis – (one feature of accrual system) (1) commitments

(2) Unencumbered balance

(3) Cash payments

(4) Unexpended balance

Re: the Bookkeeping system, also need the following:

Pre-Audit by clerk purchases legal, amount is right, like administrative audit in Fed. Gov’t; an executive & not legislative function.

Financial Reporting by Clerk – Monthly statement “Overdraft Problem” should have power to refuse payment of overdraft problem.

Post Audit – to legislative body, Post leg. & (unreadable wording) power little distinguished in County Gov’t. By private form, or by State Tax Commission.

(Supplement to the Humbird Enterprise, Saturday, September 6, 1941)

|

© Every submission is protected by the Digital Millennium Copyright Act of 1998.

Show your appreciation of this freely provided information by not copying it to any other site without our permission.

Become a Clark County History Buff

|

A site created and

maintained by the Clark County History Buffs

Webmasters: Leon Konieczny, Tanya Paschke, Janet & Stan Schwarze, James W. Sternitzky,

|

{kind=link}